Approved for Investment. Unprepared for Delivery.

Why system responsibility disappears once capital is committed

Large-scale energy transition programmes rarely fail at the point of investment approval. They pass investment committee scrutiny supported by robust financial models, negotiated contracts and clearly articulated risk allocations. Sensitivities are run, downside cases examined and mitigation strategies documented. At the moment of financial close, projects are deemed bankable, compliant and ready to proceed.

Yet many programmes that are bankable on paper encounter strain during delivery.

The gap between approval and execution is not primarily analytical. It is structural.

Investment approval processes are designed to assess whether capital can be absorbed under defined assumptions. They test counterparty credibility, price construction risk, evaluate revenue projections and ensure contractual coherence. From a financial perspective, they render an asset legible.

What they do not assign is responsibility for how the system behaves once capital is committed and multiple institutions begin to act independently.

At financial close, a project ceases to be a model and becomes a live system. Ministries, regulators, utilities, financiers, contractors and operators begin to move within their own mandates and timelines. Decisions start to interact. Incentives diverge. Interfaces multiply. Authority, however, remains bounded within contractual silos.

Responsibility becomes distributed; system-level accountability does not.

This distinction is increasingly consequential as energy transition scales.

Global reporting underscores the magnitude of the coordination challenge. The International Energy Agency has warned that achieving climate and energy security objectives requires not only unprecedented investment in clean generation but a parallel expansion of enabling infrastructure — including transmission, flexibility mechanisms and grid modernisation. In its recent outlooks, the IEA has emphasised that grid investment must rise significantly this decade to prevent bottlenecks that could delay or undermine clean energy deployment.

Similarly, IRENA has consistently stressed that system integration and institutional adaptation are prerequisites for high renewable penetration. Technology costs have declined rapidly, but institutional frameworks often evolve more slowly. The implication is clear: bankable assets alone do not guarantee coherent systems.

Yet investment approval mechanisms remain primarily asset-focused.

Consider the structure of a typical large-scale energy transaction. Generation capacity is procured through competitive tender. A power purchase agreement is negotiated. Financing is structured based on forecasted revenues under defined market conditions. Construction contracts allocate delivery risk. Regulatory approvals are secured.

Each component is analysed rigorously. Each counterparty’s obligations are defined. The project reaches financial close.

What remains unassigned is authority over system-level behaviour.

Who is responsible for ensuring that transmission reinforcement proceeds in alignment with generation deployment? Who holds authority if regulatory adjustments required to monetise flexibility lag behind commissioning? Who intervenes if tariff reform required for cost recovery encounters political resistance? Who manages the interaction between multiple concurrently financed assets operating within a constrained grid?

These questions are often acknowledged implicitly. They are assumed to be managed “through coordination” during implementation. In practice, they sit between mandates.

Capital discipline has matured. System discipline has not.

This gap becomes binding at scale. The larger and more interconnected the programme, the greater the exposure to interface risk. A project may be individually bankable while the broader system into which it is introduced remains institutionally fragile.

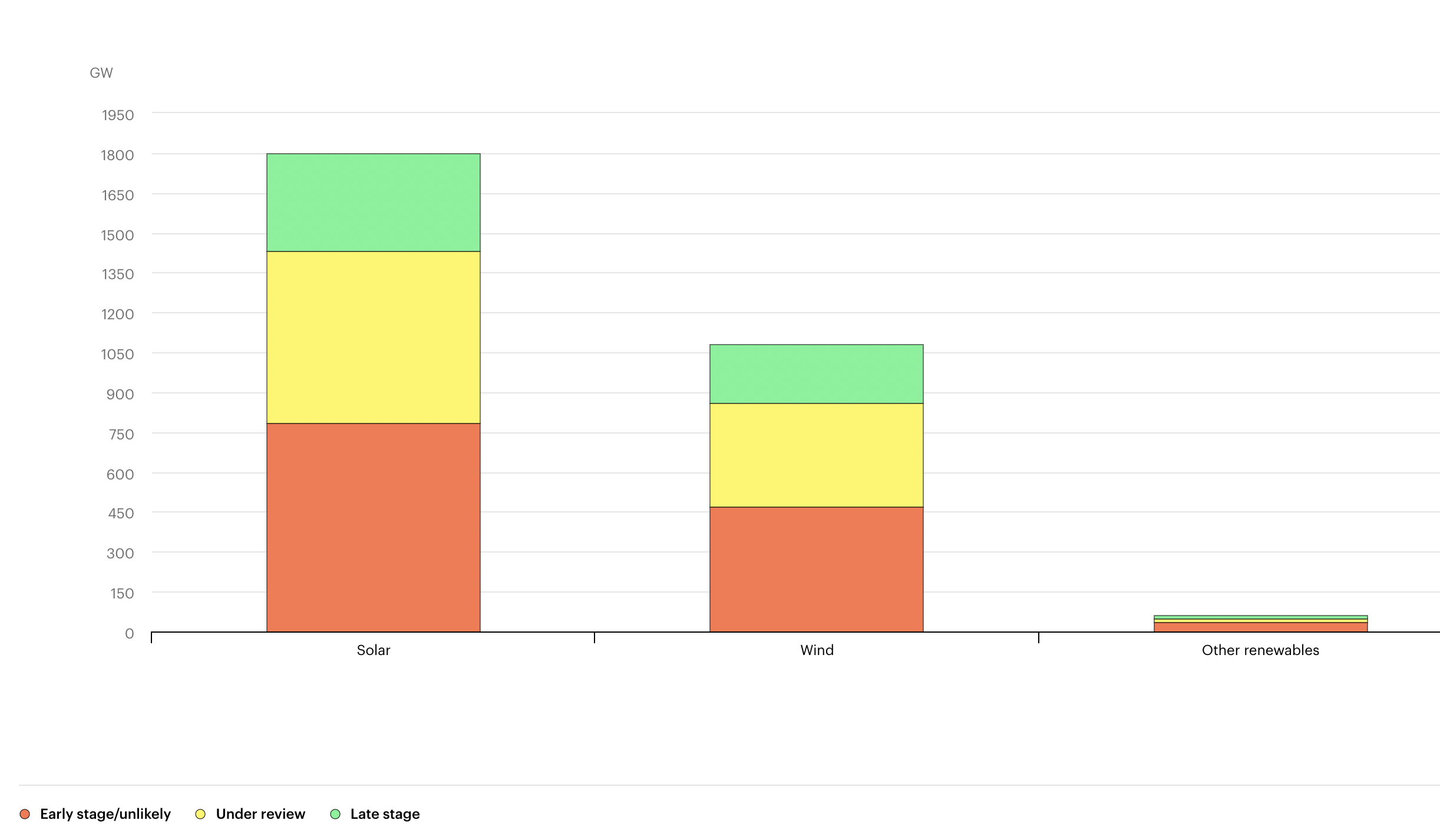

Evidence of this dynamic is visible in connection backlogs and curtailment trends in multiple advanced markets. In several jurisdictions, renewable and storage projects have secured financing and reached advanced development stages only to encounter prolonged grid connection delays. Interconnection queues in some regions now represent capacity volumes comparable to existing installed fleets.

Global renewable capacity waiting in grid connection queues now exceeds installed capacity in many markets — highlighting that the constraint is not capital availability or equipment performance; it is system absorption capacity.

Source: International Energy Agency (IEA), Capacity of renewable energy projects in connection queues, 2024

Once capital is committed, restructuring becomes costly.

Investment committees evaluate risk ex ante. They do not hold ongoing authority across institutional boundaries ex post. Ministries may sponsor programmes, but fiscal mandates limit their ability to intervene once contractual frameworks are fixed. Regulators safeguard market stability, but may lack authority to realign sequencing across assets already financed. Utilities manage grid operations, yet often do not control the pace at which generation capacity enters the system.

No single actor is mandated to hold the system as a whole.

The result is not immediate failure. It is friction.

Curtailment increases when transmission reinforcement lags. Revenue volatility rises when market rules evolve after assets are financed. Cost recovery becomes politically sensitive when tariff adjustments trail capital deployment. Investors respond by increasing required returns or delaying subsequent commitments. Replication slows.

From the perspective of capital providers, the distinction between bankability and deliverability becomes material. Infrastructure finance depends not only on asset-level risk allocation but on institutional durability. Long-duration capital prices regulatory stability, tariff credibility and system coherence over decades. When authority over system-level alignment is diffuse, that durability appears less certain.

This does not imply that investment processes are flawed. On the contrary, they are often rigorous and sophisticated. The issue lies in what they are designed to evaluate.

Bankability tests whether an asset can stand. Deliverability tests whether a system can sustain.

The two are not interchangeable.

Energy transition at sovereign scale is no longer a portfolio of isolated assets. It is an interdependent programme spanning generation, storage, transmission, demand growth, digital integration and market reform. As interdependence increases, the cost of unassigned authority increases with it.

Sequencing discipline, discussed in prior analysis, depends on someone holding responsibility for interfaces. Without explicit authority to align timelines, manage divergence and intervene across institutional silos, sequencing degrades into reactive adjustment.

By the time misalignment becomes visible — through construction delays, regulatory disputes or fiscal strain — capital is already committed and contractual flexibility limited.

Assigning system-level responsibility does not require additional bureaucracy. It requires explicit mandate. A defined authority capable of intervening when institutional incentives diverge. A function tasked not with approving assets, but with safeguarding coherence across them.

Where such authority exists, misalignments surface earlier. Transmission sequencing is treated as a design variable rather than an afterthought. Market reforms are synchronised with asset commissioning. Tariff adjustments are modelled within broader fiscal frameworks. Capital exposure is reduced because systemic friction is addressed upstream.

The cost of establishing this discipline is modest relative to the cost of post hoc correction.

The World Bank and other multilateral institutions have increasingly highlighted institutional capacity and governance quality as critical determinants of infrastructure performance. As programme complexity rises, the importance of clear authority structures grows correspondingly. Financial close is not the end of system design; it is the beginning of system exposure.

The next phase of global energy transition will test whether institutional frameworks evolve alongside capital deployment. Where bankability continues to be treated as a proxy for deliverability, friction will accumulate. Where system responsibility is explicitly assigned and empowered, acceleration will become more durable.

Energy transition finance has matured rapidly over the past decade. Contractual structures have become more sophisticated. Risk allocation has improved. Capital pools have deepened. Yet the structural question remains unresolved: who owns the system once capital is committed?

Until that question is answered clearly, bankable assets will continue to encounter delivery strain not because they were poorly modelled, but because the system into which they were introduced lacked accountable stewardship.

Bankability is necessary.

Deliverability is institutional.

As energy systems grow in scale and interdependence, the distinction becomes decisive.