Energy Systems Under Fire

Why modern energy systems must now be designed for disruption

Energy systems rarely reveal their structural weaknesses during periods of stability. They reveal them during shocks. The latest escalation in the Gulf is a reminder that the global energy transition is not unfolding in a vacuum of policy targets and technological ambition. It is unfolding within a geopolitical environment where infrastructure, supply chains and energy markets remain deeply exposed to disruption.

For planners, investors and policymakers, the central question is therefore not simply how markets react to conflict. The more consequential question is whether modern energy systems are architected to absorb shocks without cascading economic consequences.

Few examples illustrate this exposure more clearly than the Strait of Hormuz. Roughly one fifth of globally traded oil and liquefied natural gas passes through this narrow maritime corridor, making it one of the most strategically significant energy chokepoints in the world. Even the perception of disruption in the Strait reverberates immediately through global markets, because the system still relies on a limited number of physical nodes connecting concentrated extraction regions with global demand.

This dependence reflects the historical architecture of the energy system itself. Hydrocarbon resources are geographically concentrated while consumption is widely distributed. Infrastructure networks — pipelines, export terminals, refineries and maritime routes — bridge that imbalance. When one of those nodes is threatened, the consequences extend far beyond the immediate region. Despite the accelerating pace of the energy transition, the global system continues to depend on a small number of fragile infrastructure corridors.

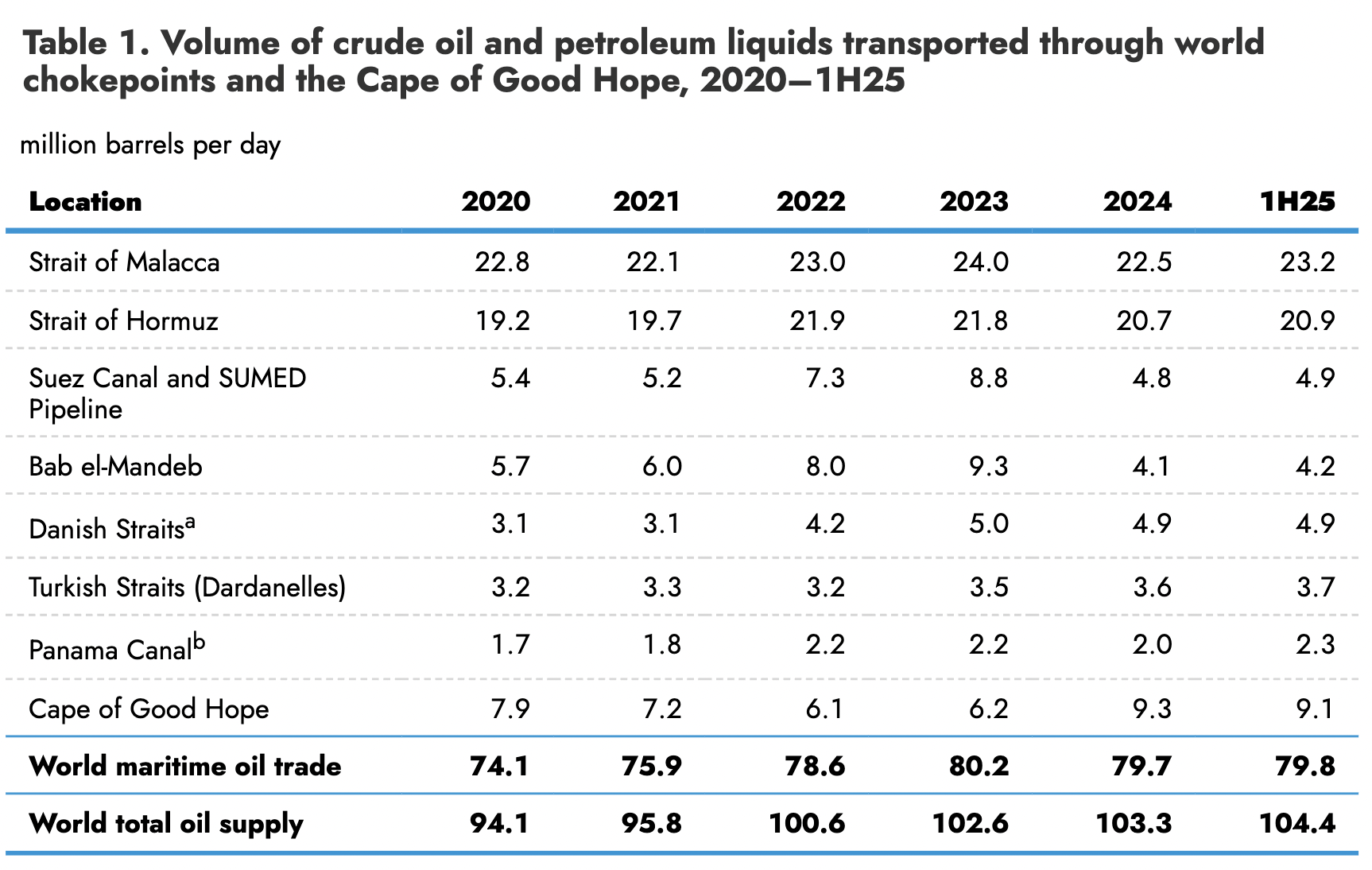

This structural exposure is reflected in the scale of global maritime energy trade itself. According to the U.S. Energy Information Administration, roughly 79.8 million barrels per day of petroleum and liquids moved through global seaborne routes in the first half of 2025 alone, representing around three quarters of total global supply.

As Table 1 illustrates, the concentration of energy flows through these narrow corridors means that even temporary disruption can force shipments onto far longer routes, increasing transit times, shipping costs and ultimately global energy prices.

— U.S Energy Information Administration (EIA), Short-Term Outlook, February 2026

Markets react instantly. Infrastructure cannot.

Within hours of the latest escalation, oil prices surged as traders repriced geopolitical risk, tanker traffic patterns shifted and insurance costs for vessels operating in the region rose sharply. Financial markets move at the speed of information. Infrastructure moves at the speed of engineering. Pipelines cannot be rerouted overnight, export terminals cannot relocate, and power systems cannot suddenly replace disrupted fuel supply with alternative capacity.

Energy infrastructure is inherently capital-intensive, geographically fixed and slow to adapt. This mismatch between the speed of markets and the inertia of physical systems remains one of the defining vulnerabilities of the global energy landscape.

Recent events have also underscored a reality that energy planners must increasingly confront: energy infrastructure has become a strategic target. Missile and drone attacks have repeatedly struck oil facilities, gas processing plants and export terminals across the region. These assets are no longer merely economic infrastructure; they are instruments of geopolitical leverage. Disrupting them can destabilise economies, influence global markets and alter strategic calculations.

Yet the vulnerability does not stop at pipelines, refineries or export terminals. Modern energy systems are now inseparable from digital infrastructure. Grid management, electricity dispatch, pipeline monitoring and energy trading all depend on complex digital networks. At the same time, the digital economy — from financial systems to cloud computing — depends on reliable electricity supply. The increasing interdependence between energy systems and digital infrastructure means disruption in one domain can cascade rapidly into the other.

In an electrifying world, energy infrastructure is no longer purely physical. It is digital, networked and deeply interconnected.

The energy transition does not eliminate vulnerability; it changes its shape. Electrification and renewable generation can reduce reliance on imported fuels, but they introduce new dependencies in their place. Grid resilience, transmission capacity, digital security and global supply chains for critical materials become increasingly central as energy systems evolve. The locus of risk therefore shifts from fuel supply toward system architecture.

This is the lesson policymakers must increasingly confront. Decarbonisation strategies often focus on the speed of deployment — how rapidly new capacity can be built and how quickly emissions can fall. Yet speed alone does not produce resilience. Systems optimised solely for efficiency during stable conditions can become fragile when exposed to disruption.

Resilient energy systems must therefore be designed with disruption in mind. That means diversifying infrastructure routes rather than relying on single corridors, building grid flexibility capable of absorbing supply shocks, strengthening cybersecurity across increasingly digital networks, and developing governance frameworks capable of coordinating responses across complex systems.

For most of the twentieth century, energy security was largely defined by access to fuel. In an electrifying world that definition is expanding. Security increasingly depends on the resilience of interconnected systems — electricity networks, digital infrastructure, industrial supply chains and the institutional structures that govern them.

A system capable of delivering energy cheaply but unable to withstand disruption is not secure.

The global energy transition is often described as a technological transformation driven by innovation, investment and policy ambition. In reality it is unfolding in a world defined by geopolitical competition, infrastructure vulnerability and accelerating interdependence. The latest escalation in the Gulf is not an anomaly. It is a reminder that the energy systems of the future will operate in an environment where shocks are inevitable.

The systems that succeed will not be those designed for stable conditions.

They will be the systems that continue to function when disruption arrives.